Put your Bitcoin to work with this guide!

Leverage the advantages of Bitcoin, but be smart about it.

As you accumulate more Bitcoin it will become more tempting to do something with it. Especially once you approach retirement.

I believe being in crypto is about maximizing your quality of life over time. Therefore, that Bitcoin in your wallet has to serve a purpose one day!

This guide is here to help you with that and set you up for success.

Let’s get the basics right first:

Nothing beats Bitcoin on its native chain. It’s the most decentralized network on the planet. No one can top that. Therefore, if you are risk adverse, best to never move your BTC from that network until you really have to.

If you plan to retire rich with Bitcoin, you need to learn how to navigate Decentralized Finance (DeFi). There’s no better time to start than today! Do it now, rather than at 65.

You do not have to use a lot of money or even Bitcoin to start learning. Use small amounts and increase them only as you get more comfortable with DeFi. Use Rabby wallet when you do, see the link with my guide why.

Don’t do it alone, join us on Discord, and consider an upgrade to a Patron role to 10x your learning curve with like-minded members.

Today, any DeFi on Bitcoin is mostly a scam. It may change later, but for now, the best place to start is on Ethereum, the second most decentralized network after Bitcoin.

Decentralization matters and this is why Ethereum is the second biggest cryptocurrency by market cap and hosts a DeFi ecosystem valued at $50 billion. Until a better alternative arrives, we continue this guide with Ethereum.

The native Bitcoin network cannot host DeFi applications because it lacks the smart contract capabilities that require that. This is why any solutions to use Bitcoin in DeFi entails a centralized entity.

This is where risk enters the picture.

In the case of Ethereum, that usually means a centralized custodian that takes your Bitcoin on the native chain, locks it, and holds it for you while it issues in return an Ethereum token of equal value (in principle).

A good example is wBTC or wrapped Bitcoin on Ethereum (an ERC-20 token).

BitGo, the custodian, holds that Bitcoin in multiple BTC addresses which can be publicly audited and in exchange issues the equivalent number of wBTC tokens to users happy to explore DeFi.

Everything went well until now and wBTC market capitalization reached $9.4 billion. They had the first mover advantage. Understand that someone at BitGo holds the keys to those Bitcoins as collateral for all wBTC issued to date. We trust them to never run with the keys.

We also trust them to never:

lend that BTC to others behind our backs

borrow USD against that collateral, or

leverage those positions in some form like Celsius or FTX did (they gambled with users money)

A lot of trust is involved. But wBTC and BitGo legal set-up makes that extremely unlikely. Anyone can check if there is enough BTC to back wBTC issued by BitGo at any time of the day. The same cannot be said of other custodians.

This is why, when you choose a Bitcoin derivative to do DeFi with, do your due diligence! Only trust reputable protocols and custodians. If anything is unclear or there is room where they can use the BTC for other purposes - run.

As soon as anything goes wrong, like someone stealing part of the collateral, the derivative token (wBTC or similar) will lose its parity to the BTC price. It will crash and won’t recover until all collateral is accounted for.

Interestingly, there has been some recent drama related to wBTC because BitGo are changing their custodian set-up in the coming months and Justin Sun (Tron CEO) will be involved in some capacity (a red flag). Why the drama?

Justin loves to use collateral to issue new money and then he takes the collateral away. That included issuing fake wBTC on Tron network against unknown BTC reserves on Poloniex, an exchange he bought. Without transparency, the wBTC issued by Poloniex crashed versus Bitcoin.

In a way, even calling it wBTC was misleading, because it was not issued by BitGo. Poloniex has since removed wBTC from their site. Clearly, there’s reasons to be concerned and monitor this closely.

Competitors to wBTC jumped quickly at this opportunity to capitalize on the drama. This includes Coinbase that announced their latest BTC derivative called cbBTC. Be careful, because most of these alternatives are likely worse since they lack transparency. As far as I can tell, there is no good alternatives to wBTC today in DeFi.

Coinbase is already promoting their cbBTC token, but they never disclosed their exchange reserves. If they have the same approach with cbBTC, stay away.

In any case, for the purposes of this exercise, you can use wBTC because it is the most widely used in Ethereum’s DeFi ecosystem.

To get wBTC all you need to do is swap your BTC for wBTC or simply buy some. On a centralized exchange it is quite straight forward. Deposit BTC on Bitcoin network and withdraw wBTC on Ethereum network (or other networks) after the swap. Takes 10-15 minutes in total. If you got stables, just buy wBTC.

If you want to do a swap using DeFi you will likely pay much more (can vary) and need to wait over an hour. Here is an example using THORChain swap. It takes 80 minutes and about $200 for 1 BTC swap. This is because you’re using native chains (BTC is quite slow) and intermediaries will add their fees.

Generally, try to use decentralized exchanges because you need to learn how that works and it also helps protect your privacy better. For example, try buying some wBTC using DeFi exchanges like Uniswap.

Once you have wBTC on Ethereum (or other networks), the crypto world will offer many opportunities to put that (fake) Bitcoin to work. Remember, the real Bitcoin is held by BitGo in your name on the BTC network (or rather under the name of the vendor that sold wBTC to you).

The most obvious choice is to borrow stablecoins against your wBTC on AAVE or similar lending protocols. You add your wBTC as collateral and earn 0.08% interest on that and you borrow USDC at 5.72% interest. Easy right? But why would you do that?

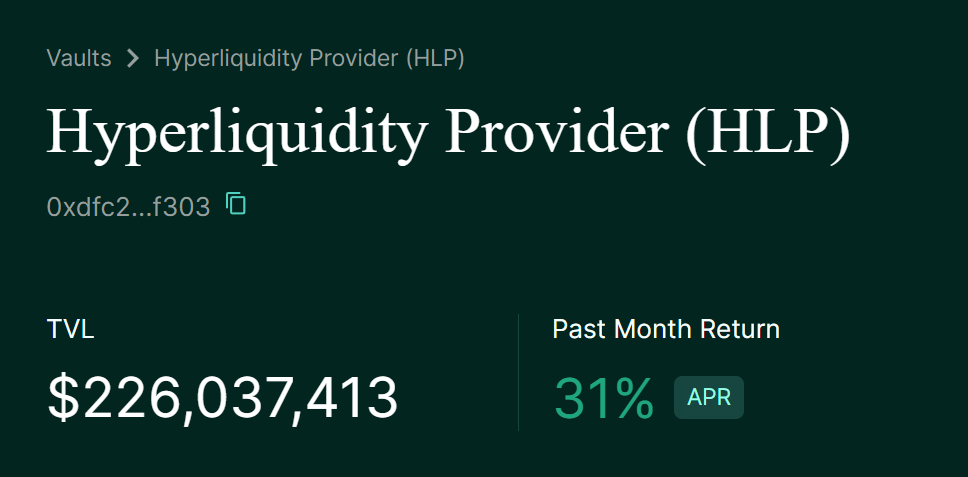

Because you keep your exposure to Bitcoin (assuming its price goes up over time) if you need cash. Or you can farm 30% APY on USDC using Hyperliquid. That’s plenty to offset that 6% interest on AAVE.

This is where you need to control greed and borrowing rates. Watch those liquidation levels and assume a 50% crash in BTC’s price as likely.

You see, there are many exotic protocols ready to take that wBTC. But most of them will likely crash with your money stuck there. Kujira is a recent example and they also accepted BTC derivatives.

Be very picky where you put your wBTC to work. Don’t trust any APY that is unclear how it is generated. The more confused you are, the more you should run away.

Thing is, DeFi is scaling down. Think of BTC and ETH as the base layers in an inverted pyramid. As you go deeper, liquidity shrinks, decentralization becomes less important, and risks increase. The lower you go, the less resilience you’ll find because liquidity is more limited to absorb market shocks at those levels.

A good example of DeFi on Layer 2 is GMX. This decentralized exchange is on Arbitrum, a sub-network of Ethereum. There, you can put your wBTC to work in their trading pools used by their traders or users. The wBTC APY is 8% right now.

This is a good alternative to borrowing against your wBTC. Instead of paying AAVE 6% for that privilege, you get paid 8% by GMX for the liquidity you provide to their users. It’s not risk free, but it’s pretty close to that for such returns.

On the other hand, Hyperliquid is actually on Layer 3 (Ethereum > Arbitrum > Hyperliquid). It trades security and decentralization for speed and low fees. Anywhere on Layers 1 to 3 you need to manage risks properly and see what you are comfortable with.

Try to master the networks first and understand where your money is actually sitting before you dive into the protocols, individual projects, and their risks. As the DeFi market matures, there will be more and more opportunities to use your Bitcoin with a favorable risk/return rate, all things considered.

One day you’ll need to put that Bitcoin to work and capitalize on its benefits to improve your quality of life. That can mean simply selling it (which I don’t recommend), using it to generate yields (the smart way) or borrow stablecoins in perpetuity (the smartest way).

Since 2011, Bitcoin doubled in price on average every year. That’s more than enough to forever pay any yearly interest on stabelcoins when you retire. Just don’t be greedy and watch liquidations levels if you take that route.

At the end of the day, the best custodian of your Bitcoin is yourself! Invest in your knowledge and proficiency if you want to retire rich. And don’t hesitate to ask questions. You’ll find me on Discord for that.

This newsletter is made possible with the generous support of our community Patrons and partners. Upgrade your experience to show your support by clicking the below button or reach out to us on X or Discord to partner.

All info is provided for educational purposes only and is not financial advice.

Excellent article! Would love to hear your thoughts on Bitcoin L2s if you have the time too!