The secret ingredient to retire rich and stay rich: Bitcoin, my roadmap. #14

Bitcoin and DeFI are a match made in heaven that will allow you to retire early and live a stress free life.

In 2014, I bought my first Bitcoin at $700 during the top of that bull market. Fast forward to 2023 and I still buy Bitcoin. My latest buys were under $20,000. Why do I continue buying and will not stop?

It’s my retirement or should I say FatFIRE. FIRE stands for Financial Independence, Retire Early. Fat just means you retire rich and stay rich. Want to join me?

Here’s the roadmap for that.

The reason I advocate for Bitcoin as a FatFIRE strategy above all else is three fold:

Best risk / reward

Most liquid

Most decentralized

First, the risk reward ratio for Bitcoin is amazing on a long time horizon. You stand to 10x, 20x or 50x your money in a few decades. A small investment today can be a significant - life changing money - tomorrow. This cannot be understated.

Second, Bitcoin is also the largest cryptocurrency by market capitalization. As time passes, this is expected to increase while at the same time, the price volatility for Bitcoin will decrease. This presents you with less risk when you will retire using Bitcoin. Less price volatility, more consistent payouts from DeFI markets.

Third, by using the most decentralized form of money ever created you are protecting your wealth and yourself from key risk factors such as: devaluation, dilution, confiscation, abuse of power, corrupt governments, and so on. You are the sole custodian of a form of money and wealth above the control of any third party or state. A quick glance at Lebanon, Turkey or Egypt is sufficient to prove this point.

Your goal is to accumulate Bitcoin in your most productive years, hold it and then put a part of it to work for you (as a liquidity provider) in DeFI markets during your retirement.

Here are just two DeFI examples you can use today. This is not a fictional future. This is actual reality. Enter the GMX and GMD protocols and their tokens. If you missed my newsletter on how to choose the right altcoins, then I suggest you read that first to understand why real yield tokens stand out and how they fit into your FatFIRE strategy.

This morning, one of my community members asked me the following question:

Where does the 20% APY come from on GMX? Sounds like Terra / Luna / UST. How do they make the money to give that APY in BTC? What are the risks?

A good question and one everyone should ask themselves. If you don’t know where the APY comes from, then it’s time to bail and never look back. Fortunately for us, in this case, we do know and it is highly transparent.

In simple terms, GMX makes money from two key streams:

Trading fees

Every time a trader opens or closes a trade they pay 0.1% in fees. If they need a different coin to open a trade, say they have ETH, but they want to short it, then they need to swap that ETH for USDC and hold USDC. That swap has a 0.2% - 0.8% fee depending on the available liquidity.

As you can probably tell, liquidity on GMX is a big deal. I’ll come back to that.

Borrow fees

If you want to use leverage on GMX, then you have to borrow that liquidity from the exchange (which is provided by GLP holders). This borrow fee is equal to 0.01% per hour per asset borrowed.

In the above example, if you plan to short 1 ETH at 10x leverage, that means you need to borrow about 13,000 USDC at today’s rates. That’s a lot of money and a lot of fees / hour. Now imagine that traders borrow millions every day. It quickly adds up over time.

These fees do not go to some centralized entity to splurge on. Nope. They go to you. And in this case it means holders of GMX and GLP tokens. 100% of all fees go to these two token holders. This is what real yield means.

The payout split is 30% to GMX (governance token) and 70% to GLP (liquidity providers). What type of liquidity? Mostly BTC, ETH and USDC. See the below picture for a clear breakdown of the assets backing GLP. For comparison sake, the Terra stablecoin UST was backed by nothing and had a 20% APY which was also worth nothing because it was paid in… UST. GMX fees are paid in ETH or Avax.

By holding GLP, you can be one of those liquidity providers and earn 70% of GMX fees which currently has an APY of about 20% (keep reading). That’s a lot of trading, right? What convinced me was the below chart.

It shows that GLP holders pretty much went through this bear market without a scratch (check the blue line). The value of their GLP did not decrease! Yes it was volatile, but it was much better than 99% of the market during the same period thanks to the fees accrued.

If that does not impress you, then probably the next image will. You see, the problem with GLP is that you also hold other assets, not just Bitcoin. You are exposed to Ethereum volatility, USDC and a few other altcoins (albeit with a very small allocation).

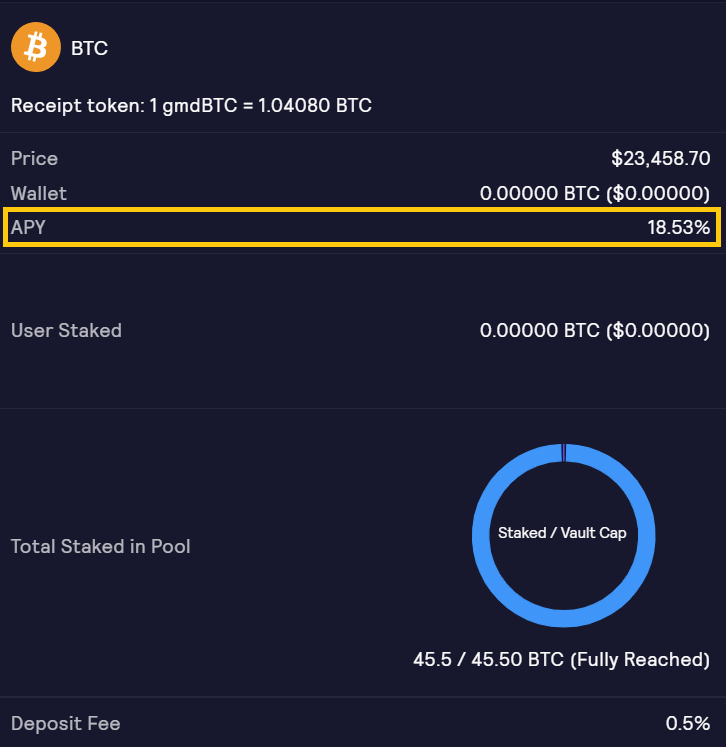

If you plan to FatFIRE, then you should hold and use Bitcoin as indicated at the start of this newsletter. GMD fixes this by giving you exactly that solution. You can hold only BTC and accrue almost the same APY. The GMD protocol is build on top of the GMX exchange and their added value is to offer vaults that expose you to only one type of coin, based on your risk profile. In this case, we choose BTC and as you can see below, their vault is sold out.

As the protocol grows, there will be more room to join, but this won’t last. At some point, those that hold GLP or BTC in the GMD vault will be a very exclusive group. GMX can only scale and keep that 20% APY if they maintain a good balance between trade activity on their exchange and liquidity size. So far they did a great job.

My point is, there is not enough room for everyone. Expect to see such vaults and those liquidity pools on GMX being sold out constantly.

Nevertheless, DeFI and crypto is an expanding, growing market. This will offer plenty of alternatives and opportunities to put your liquidity to work. But you need to be extremely careful who you choose to trust with your money. I do not recommend putting all your BTC liquidity into DeFI. Most should probably be held in a cold wallet for safe keeping.

Above all, make sure you retain full custody over your assets at all times and there is no lock-up period. This means you can trade in and out as you please, when you please. I covered other risks in my Twitter thread at the start of this newsletter.

What is important to remember is that as your BTC holding grows (in value and size), the APY that you will require in retirement to maintain a steady (and substantial) income stream will be lower. A lower APY also means a lower risk profile when you will provide liquidity later. Therefore, building a strong foundation today will put you in a very privileged position in the future to choose a robust DeFI protocol that has fewer risks.

The elephant in the room will say that the above assumes one thing - the success of Bitcoin over the coming decades. My answer to that is quite straightforward. You do not have a better alternative right now. If you do, drop it in the comments to this newsletter. Bitcoin also has the best track-record since 2009. It’s in a class of its own. Even the US SEC admitted that (pictured).

From a purely risk/reward angle, based on all the information we have today, Bitcoin is your best bet to an early retirement that will allow you to live a fat life, stress free. Therefore, only one question remains. 👇

Hey you,

If you enjoyed the above, I invite you to be part of my community and share this newsletter. If you want to learn more about YCC, head to the About page.

To get started on your crypto journey use one of my referrals (scroll down on the link) and then consider becoming a Patron. You can find me on Discord for any questions and if you want to start a collaboration, reach out!

Don’t forget to follow YCC @ Twitter ◇ YouTube ◇ TradingView

Yours,

Duo Nine - YCC Founder

Love it. Thanks for this kind of guide and all information. I hope to get into DeFI and those pools/vaults anytime soon. There is a reason why they are sold out pretty fast.

🤍